Financial markets always seem to be in flux and every year brings surprises as well as the confirmation of some emerging themes. This year is no different as investors have had to battle with a number of issues such as the continued energy complex meltdown, a potential interest rate hike in the US, a weather related slowdown in US economic growth, the strength of the US dollar, the rocket-like ascent and subsequent coming down to earth performance of Chinese equities and most recently the continued travails of the Euro Zone precipitated by the debt crisis in Greece.

Financial markets always seem to be in flux and every year brings surprises as well as the confirmation of some emerging themes. This year is no different as investors have had to battle with a number of issues such as the continued energy complex meltdown, a potential interest rate hike in the US, a weather related slowdown in US economic growth, the strength of the US dollar, the rocket-like ascent and subsequent coming down to earth performance of Chinese equities and most recently the continued travails of the Euro Zone precipitated by the debt crisis in Greece.

In general, most fixed income strategies exhibit year-to-date losses while most equity indices stand in positive return territory. Non-US developed equities in particular have performed well. Small caps have also out-performed globally. Interest sensitive assets such as REITS and higher yielding equity segments have under-performed while commodities continue in the doldrums. Investors shying away from commodity and interest sensitive sectors as well as those willing to hold significant international equity exposure have been rewarded thus far in 2015.

Major broad equity market indices tell a fairly benign story thus far in 2015. Volatility has been low and the hiccups when they have come have been short-lived and muted.

Just like watching a live play hides the beehive of activity going on backstage, broad indices often obfuscate the myriad of developments and emerging themes shaping up in smaller pockets of the global equity markets

Let us take a closer look at global equity market performance thus far in 2015. Our universe is comprised of over 14000 stocks distributed over 50 plus markets. As you can imagine, in such a large universe we will have spectacular successes as well as failures and we, therefore, rely on median local currency returns as our barometer for performance.

Return averages are too subject to outliers and medians, while simplistic at first blush, give us a reasonable sense of performance across countries, economic sectors and investment characteristics.

We also choose to focus our analysis on local currency median returns as we believe that mixing currency and local stock performance (putting everything in, say, US dollars) can sometimes lead to erroneous inferences regarding the strength of certain trends.

Suffice it to say that this year the vast majority of major currencies have depreciated versus the USD resulting in lower equity returns to non-US strategies from a US-based investor perspective.

For our sample of global equities the median local currency return stood at 8.9% through July 3, 2015. The average return (once we trim obvious outliers) came in at 13.5% denoting some positive skewness in the return data. The median USD-denominated return for our sample was 6.7% highlighting the first half strength of the currency.

Drilling Down By Geography:

Let us start by drilling down by geography as shown in Figure 1. The first thing to notice is that very few markets (Colombia, Greece, Indonesia, Mexico, Peru and Taiwan) have had negative median returns this year.

Second, some lesser travelled markets such as Argentina, China, Czech Republic, Hungary and Russia have thus far excelled in 2015 with median local currency returns north of 20%. Other notable performers typically in the wheelhouse of global investors include Denmark, Italy and South Korea.

Figure 1

If you are having trouble finding the US that is because the median US stock has had a paltry 2% return in H1. Nothing to write home about compared to most other global equity markets.

What about all the fuss regarding the rebirth of Japanese stocks? To me it still seems justified given the 13% median return to Japanese equities in 2015. In fact, the larger international markets have all outperformed the US with median returns several orders of magnitude larger (UK stocks are up 9%, German and French stocks are up 15%).

A Further Look by Economic Sector:

A look at median returns broken down by economic sector (Figure 2) reveals the continued struggles of the more commodity and interest rate sensitive segments. The only sector in the red for 2015 is Energy while the Non-Energy Minerals aggregate is barely positive for the year.

Commodity exposure continues to be shunned by investors living in today’s low inflation environment. Interest sensitive sectors such as Utilities and Telecom have also suffered from the upward drift in yields (especially in Q2) and the perception that a sequence of interest rate hikes by the Federal Reserve and possibly the Bank of England are just round the corner.

On the positive side, the growth oriented sectors have had superior performance in 2015. Anything related to information (primarily software) and health care technology has done well this year.

On a surprising note has been the performance of the Process Industries sector (this includes primarily Chemical companies with a smaller representation of Paper and Food). These industries are the direct beneficiaries of lower commodity prices (their production input) but in all fairness as we dug through the sector we found a high proportion of smaller cap rocket stocks in countries such as China, South Korea and Germany.

Figure 2

One Last Peek – A Bottom-Up Stock Perspective:

Country and sector affiliations have historically been key drivers of stock performance but stock selection has typically been where most of the action takes place. Some of that stock specific contribution is clearly random while another piece of the pie is driven by the bottom-up characteristics of the stock. These characteristics are sometimes referred to as styles (for example growth or value) and at other times as factors. Yet another set of terminology has emerged in the last few years as the industry has re-labelled several of these stock characteristics as “smart” beta.

For purposes of evaluating stock characteristic performance we employ the same universe of global stocks used previously. However, instead of aggregating stocks by geography and sector we create membership buckets (with data as of year-end 2014) according to the value of the characteristic in question. For example, we split our entire sample into 10 buckets (Deciles) according to the price to earnings ratio of stocks ranking them from low (Most Attractive) to high (Least Attractive). Decile 1 thereby contains the most inexpensive stocks in our sample. We proceed to create analogous deciles for a range of stock characteristics typically employed by fundamental and structured portfolio managers alike.

We categorize our stock characteristics into the fundamental concepts of valuation, growth, profitability, income generation, and capital structure. We supplement these fundamental drivers with analyst and investor sentiment along with two “smart” beta factors (low volatility and market capitalization).

Table 1 outlines the specific stock characteristics we analyzed as well as the rationale behind their selection while Figure 3 highlights the spread in local currency median returns between the top three deciles (Most Attractive) and the bottom three deciles (Least Attractive).

Table 1

If the market behaves according to conventional wisdom (as outlined in the table) the spread in performance should be positive. For example, if we believe that cheaper stocks outperform expensive stocks then the return spread should be positive. All factors have been aligned so that Decile 1 contains the most attractive stocks and conversely Decile 10 contains the least attractive members.

A quick glance at Figure 3 confirms that the real world of global equity investing is frequently messy. The good news is that a significant number of our stock characteristics led to performance spreads in the right direction (recall that our expectation is that all the bars in Figure 3 should be positive).

The reality of global equity markets during the first half of 2015 was, however, not kind to valuation approaches as shown by the mostly negative spreads. Take a look at the leftmost bar which corresponds to the spread in performance between the cheapest and most expensive stocks in terms of price to earnings ratios (PE). The return spreads is -4% meaning that the strategy of buying low PE stocks and going short high PE stocks would have cost you 4% thus far in 2015. The only valuation indicators with a positive return spread were Price to Sales (PS), Enterprise Value to Sales and the PEG ratio (growth adjusted PE).

Companies reducing their share counts the most underperformed (SHARES_OUT) during H1 2015 as did lower volatility stocks (VOLAT). In addition, the momentum effect (TRY1_LOC) was very strong during the first half of the year. The momentum spread was over 9% and the relationship was monotonic across all deciles. The top decile for momentum had a median return of 15.5% while the bottom decile yielded a median return of just 1.6%.

In terms of market capitalization small caps widely trounced large caps as shown by the over 8% median return spread. Most of the outperformance of small caps was driven by the smallest group of companies (Decile 1) which were up a median return of 29%. Active equity managers tend to frequently possess a capitalization bias (favoring smaller caps) that should have proven rewarding thus far in 2015.

Figure 3

The search for income (DY) was not particularly fruitful in our sample of global equities. The return spread between the highest yielding stocks and non-payers was close to -4%. The effect was fairly monotonic indicating that the market place rewarded investors de-emphasizing the income component in their stock selection. The widely anticipated interest rate increases in Q2 derailed the competitive advantages of dividend paying stocks (relative to say bonds) and most likely have sensitized investors to the dangers of chasing yield at the exclusion of other desirable stock characteristics.

Interestingly, stocks with lower current debt burdens (DEBT_EBITDA) outperformed their more indebted peers possibly reflecting investor unease with a scenario of rising rates. The real effect of rate rises on company financial health is a function of many variables including the maturity schedule of the debt. My sense is that most savvy company managements have been eagerly extending their debt maturities at the still very attractive real rates prevailing globally. I would not expect this factor to play a major role in stock selection over the next year or so unless, of course, we dive into a global recession.

Sell-side analysts have been rewarded this year in their stock picks. While the relationship between mean analyst ratings (REC) and median stock performance is not perfectly linear (there is a bump in the middle of the distribution) analyst recommendations have proven money winners this year. This follows a generally sub-par 2014 when their mean predictions were generally un-informative.

Growth-oriented investors have enjoyed favorable global equity market developments. Most profitability measures have proven valuable as stock picking strategies(especially Return on Capital) but the real boost has come from the performance of stocks exhibiting superior growth characteristics (in terms of EPS, Sales, Cash Flow and Dividends). All the return spreads for the growth-oriented factors as shown in Figure 3 are positive and large.

High Level Summary of Research Findings:

- Value-oriented approaches have worked perversely thus far in 2015. Expensive stocks have outperformed their more inexpensive brethren. Low volatility stocks have also under-performed along with dividend paying stocks.

- Growth oriented factors along with momentum and market capitalization have provided the greatest median return discrimination within our global stock universe

- From a top-down perspective the surprise has been the strong performance of some of the smaller less-travelled equity markets

- The median return to US stocks stood at 2.2% significantly lagging the median local currency returns of other major equity markets

- In terms of economic sector median stock performance we continue to see both commodity and interest rate sensitive sectors underperform.

- Stocks in growth oriented sectors such as Health Care and Technology, on the other hand, continue to perform well in the first half of 2015

Turning Research into Insights – Finding Fundamental Themes

A big part of the challenge facing investors is turning the vast array of top-down as well as bottom-up data into money making insights. With markets always on the go and the extreme amount of noise facing investors it is tempting to adopt a purely passive approach.

A more fruitful approach might, however, be to become more discriminating about separating the everyday noise in the markets and focus instead on finding a small number of themes with a high probability of lasting power and money making potential.

Themes can be micro or macro-based. A good example of a micro theme might be the emergence of “Big Data” as an investment concept. Another one might be mobile device security. Micro themes can be especially lucrative early on but at inception suffer from a dearth of publicly available investment options.

Grass-roots fundamental research is often the only way to unearth these opportunities until they enter the mindset of Wall Street firms. Micro-themes can still remain highly profitable after their discovery by the broad investment community, but gradually expectations exceed reality and the opportunity is subject to over-pricing.

Macro themes on the other hand are more general in nature and tend to have a longer life span. There are usually a myriad of liquid investment options available to capitalize on the theme. Macro themes are usually commented in the press and their knowledge among investors is widespread. A representative macro theme might be the re-emergence of global inflation. Another macro theme might involve the breakup of the Euro.

There is usually a wide divergence of opinion when discussing macro themes. Opinion differences might revolve around the likelihood of the theme happening and its timing. In addition, the impact of the theme on capital market prices might be subject to debate.

While at any time there are usually a large number of themes circulating among investors, our preference is to focus on a small number of themes that based on our research have a reasonable probability of both occurring as well as being impactful to asset prices. We also strive to find common findings among our top-down and bottom-up research that further lend support to the theme.

Some of the themes that Global Focus Capital is trying to capitalize on fitting our research criteria include:

- The growing gap between supply and demand in the global energy market leading to continued downward price pressures

- The breakdown of the alternative yield trade as investors learn to pay attention to the associated risks and exposures of their strategies

- The shrinking profit pie and the search for secular growth investments only marginally influenced by business cycle conditions

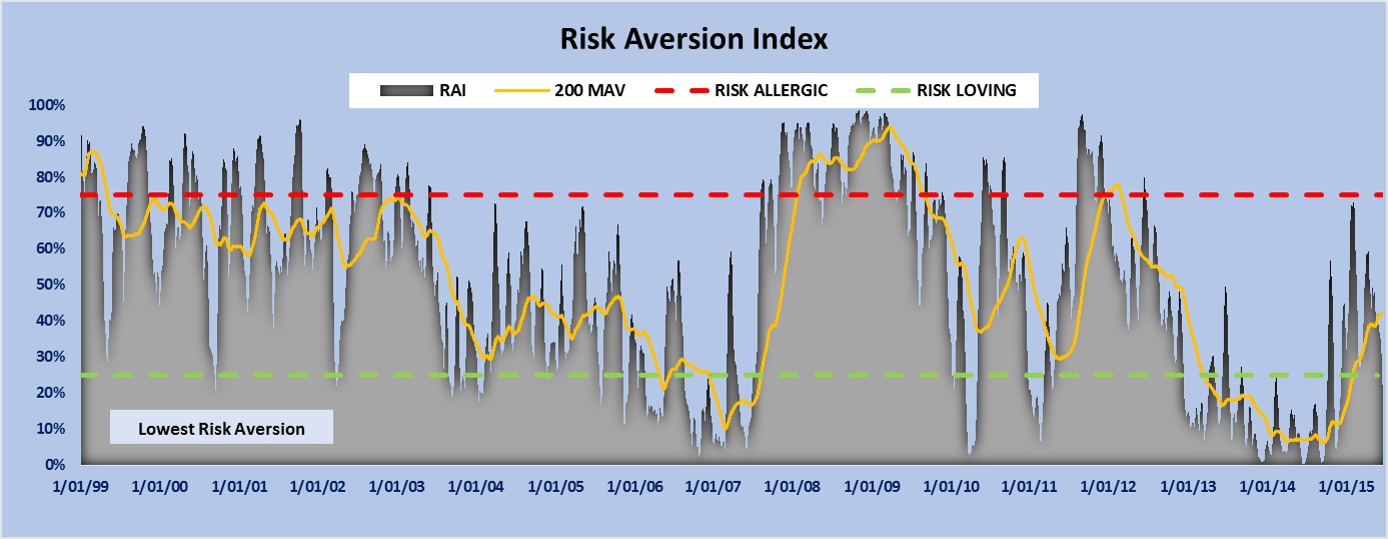

- The volatility dampening effects of highly expansionary monetary policy leading to an under-appreciation of longer term risks and potential over-leveraging

- The re-awakening of investors to global economic growth imbalances leading to periods of risk on/off in capital markets

Eric J. Weigel – Managing Partner

Feel free to contact us at Global Focus Capital LLC (info@gf-cap.com) to find out how we can help with your investment needs. Download PDF version of report.

To receive valuable reports like this by email, sign up below!