Financial markets frequently feel like the morning commute on a major city subway system. When the weather is sunny and the trains are running smoothly you are all smiles and your mood is upbeat. But, watch out if you are experiencing weather delays and personal space is compromised. Your mood and that of your fellow travelers darkens considerably and your thoughts switch immediately to how to escape the situation.

Financial markets frequently feel like the morning commute on a major city subway system. When the weather is sunny and the trains are running smoothly you are all smiles and your mood is upbeat. But, watch out if you are experiencing weather delays and personal space is compromised. Your mood and that of your fellow travelers darkens considerably and your thoughts switch immediately to how to escape the situation.

Investors likewise frequently feel this tug of war between one moment being upbeat and confident and the next being rife with doubt and stress. Back in 2009 Mohamed El-Erian then at Pimco described the changing mood swings of investors using the risk on/risk off label.

While the risk on/off concept makes a lot of sense to truly grasp the investment implications of such mood swings one needs an objective yardstick to properly identify these periods of euphoria and sheer despair.

Most of the methodologies that researchers have used to identify investor mood swings employ measures of general uncertainty regarding asset class prospective performance, credit conditions and broad macro-economic health.

The technical details separating one system from the other would put most investors to sleep, but in general my observation is that all these “investor mood” models are directionally correlated. For example, the period 2004-2006 is generally classified as upbeat while the period from 2008 through 2009 is generally described as harrowing.

At Global Focus Capital we call our proprietary system the Risk Aversion Index (RAI). The higher the RAI the more fearful investor are, or in other words the more risk averse. We calculate this measure daily and sometimes, given the rapid mood swings, we have come to think of market participants as suffering from multiple personality disorder. However, on a kinder note what we generally observe is that investor mood tends to reside, over the intermediate-term, in defined ranges of risk aversion.

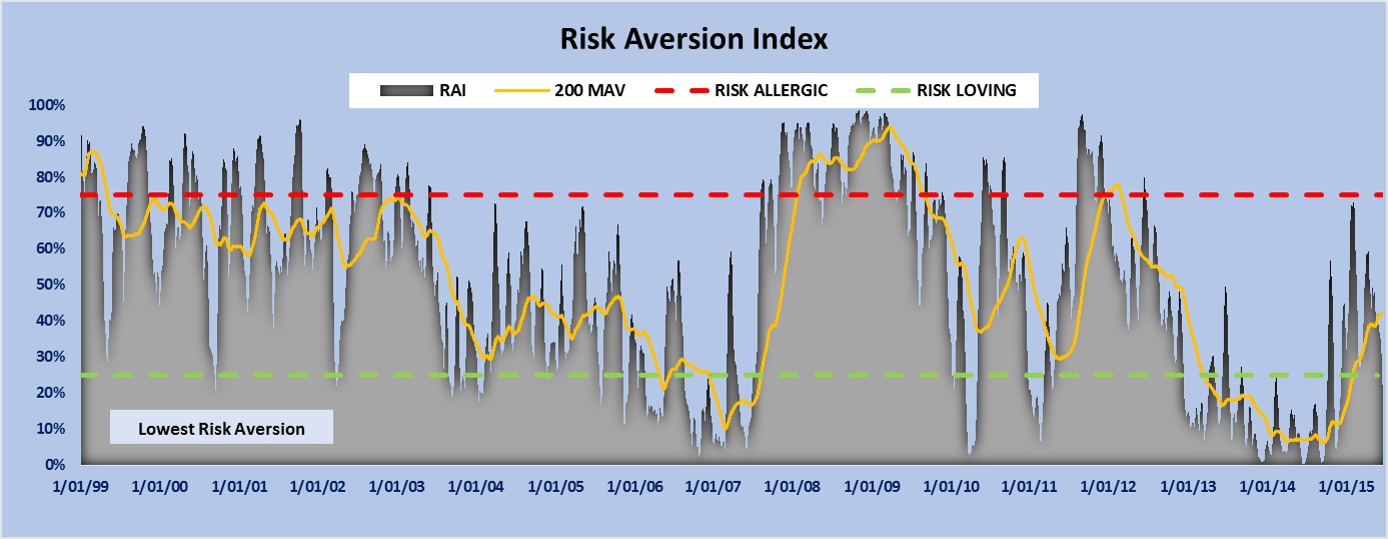

Let me illustrate what I mean by referring to Figure 1. The first thing to notice is the choppiness of the Risk Aversion Index (grey area). This clearly provides empirical support to the concept of risk on/off. Investor mood is highly volatile and switches sometimes rapidly from euphoria to despair.

The second thing to notice is the tendency over intermediate time periods to remain in a defined range of risk aversion zones. We use a 200 day moving average to smooth out the daily ups and downs and better visually this clustering effect. While investor moods are ever changing, in general, we see long periods of time when investors are much more tolerant of risk and similarly other periods when investors crave above all else for the safety of their capital.

Figure 1

Let me elaborate further. For simplicity we classify our RAI readings into three risk zones – a Risk Loving Zone (defined as the bottom 25th percentile of observations) where investors are usually dismissive of potential adverse developments and are willing to accept less return per unit of risk. The period 2013-2014 accurately describes this low risk aversion environment. Many observers would attribute this indifference to risk as a function of the very loose monetary policy of the day. Similarly the years before the 2008 Financial Crisis exhibited a strong downward trend in risk aversion.

The second zone (middle 50% of observations) labelled the Neutral Zone is the area where investors some days feel good and on others feel a bit down but in general there is a healthy balance between risk and potential return. This middle zone is one where investment strategy is preferably based on longer-term fundamentals and less influenced by the prevailing capital market risk environment.

Finally, we define a Risk Allergic Zone (top 25% of observations) where gloom and doom is the order of the day. The periods surrounding the bursting of the Tech Bubble and the Financial Crisis of 2008-2009 best illustrate occurrences when investors suffered from such a high aversion toward risk.

What does it mean to be in each one of these risk zones? Without going into all the portfolio construction issues (which we will explore in a separate note) let us just focus on returns.

In Figure 2 we illustrate average monthly returns since 1995 for the major asset classes typically part of our asset allocation strategies at Global Focus Capital. Among equities and fixed income we split the asset classes into domestic and international and also always include alternatives such as real estate and commodities.

Figure 2

Periods of capital market stress such as those when the RAI is in the Risk Allergic Zone (red bars) are difficult for investors holding riskier asset classes such as equities. In line with conventional wisdom the higher the perceived risk the more negative the average returns. When the RAI is in this zone all equities suffer but emerging markets takes the biggest hit (down 2.3% on average). Our two alternatives (Real Estate and Commodities) also take a hit but the overall negative effect is dampened due to their exposure to non-equity risk factors.

Fixed income on the other hand tends to exhibit positive average returns during this high risk aversion phase. In fact, the highest average returns of all asset classes correspond to government bonds (US and Non-US developed market). US Government bonds for example show an average monthly return of 1% in the Risk Allergic Zone.

Let’s see what happens when the RAI falls in the Risk Loving Zone (green bars). Here the situation is reversed. Asset classes with higher perceived risk tend to do better. Emerging market equities do best on average and small caps outperform large cap stocks. Real estate also does well. Within fixed income emerging market bonds do best, but in general the performance of safer assets lags significantly behind that of riskier investments.

When in the Risk Loving Zone it pays to be aggressive, but one must also be mindful of taking on too much risk in exchange for less and less potential reward. Both the Long Term Capital Management implosion in 1998 and the 2008 Financial Crisis debacles occurred on the heels of investors being highly dismissive of the risks involved. In both cases investors were taking on a disproportionate amount of risk for smaller amounts of potential return.

Finally when evaluating returns in the Neutral Zone (orange bars) it is interesting to note that, on average, equities tend to exhibit the best monthly returns when in this risk phase. All four equity classes show this tendency. Likewise real estate also shows the highest average returns in the Neutral Zone. Interestingly, the highest perceived risk asset within fixed income – Emerging Market Debt – also shows this characteristic.

Where is the RAI now and what should we be doing? Our barometer is currently entrenched in the Risk Loving Zone with a reading in the 20th percentile. The RAI has been trending up (becoming a bit more aware of risk) but despite headaches in Europe we are still seeing very low levels of risk aversion.

We suspect that the expansionary monetary policy in the US, Japan and Europe is artificially depressing capital market volatility and that the temptation to remain aggressive (and potentially take on leverage) is driven by the exceptionally low cost of money. We remain wary of too good of a thing and the quietness of the capital markets concern us. We believe that investment performance is most aligned with fundamental trends when investors display a healthy risk to return relationship such as when in the Neutral Zone.

What could trigger a change in investor mood? Potentially a whole host of issues frequently best understood in hindsight. But on a more practical note we would highlight two areas of concern. First, while highly anticipated, we think that investors will react negatively to the first increase in the Federal Funds Rate and risk aversion will jump up sharply. The second concern involves contagion effects should a Greek default occur. At the very least the interest spread between safe and riskier debt should jump up. This would lead to a higher RAI and riskier investments will likely bear the brunt.

On a final note, we believe that investment risk is being underpriced at the moment and that there is no better time to evaluate one’s willingness to trade off risk in relation to potential reward. Monetary authorities have provided investors with a nice safety cushion and allowed aggressive investors to benefit disproportionally, but the ride is nearing an end at least in the US.

Eric J. Weigel

Managing Partner

Feel free to contact us at Global Focus Capital LLC (info@gf-cap.com) to find out how we can help with your investment needs. You can also download this report in PDF format or sign up to receive future ones by email below.